The technology-driven agency execution specialist

08.11.2023

The top performing 2.4% of companies were responsible for the $75.7 trillion in net global stock market wealth creation over three decades.

Nicholas Colas, co-founder of DataTrek Research, highlighted in a blog that an academic paper, ‘Long-term shareholder returns: Evidence from 64,000 global stocks,’ has been circulating recently so DataTrek commented on the findings.

The academics analysed long-run shareholder outcomes for more than 64,000 global common stocks between January 1990 and December 2020. They found that the top-performing 2.4% of firms account for all of the $75.7 trillion in net global stock market wealth creation over that timeframe. Outside the US, 1.41% of firms account for the $30.7 trillion in net wealth creation.

In addition the majority, 55.2% of U.S. stocks and 57.4% of non-U.S. stocks, underperform one-month U.S. Treasury bills in terms of compound returns over the full sample.

“The fact that most global stocks fail to beat T-bills is, to our thinking, even more of an “aha!” observation than the fact that just a few stocks pull all the weight,” said Colas.

The top five names contributed 10% of total net global equity wealth creation on their own:

- Apple: 23.5%

- Microsoft: 19.2%

- Amazon: 31.1%

- Alphabet/Google: 19.3%

- Tencent: 48.1%

Colas highlighted that the top 20 companies were responsible for 20% of total net global equity wealth creation in the sample even though many were not public for the entire period. For example, Amazon went public in 1997.

Nicholas Colas, DataTrek Research

“Disruptive innovation is the key driver of global equity returns, and this will not change over the coming decades,” he added.

He continued that as just a relative handful of names are responsible for total long run global equity returns, the right way to think about stocks is that equity indices usually go up, but only because of a small group of names. Therefore, he recommended that traders dealing in these names should look for catalysts, set stops and take-profit levels, and avoid turning a trade into an investment.

“To match index performance over time one must have at least market-weight exposure to the handful of stocks that actually drive performance,” he added. “This is one reason why index-based investing is superior to most alternatives. The market gets things wrong, but human judgement often makes even more errors.”

Colas expects the list of long run winners will be different in the next 20 to 30 years but that US companies will still dominate the Top 20 list. So, investors should be overweighting US equities, especially in tech and adjacent industries.

“The key lesson from the current list is that disruptive innovation drives global equity returns more than any other factor,” he said. “America, with its world-leading venture capital industry, is best positioned to create the winning companies of the future.”

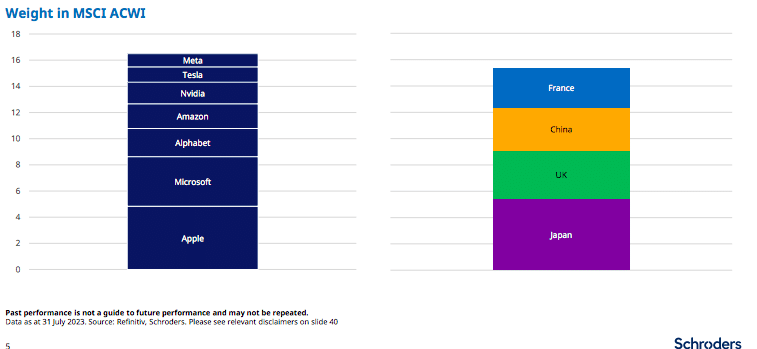

The performance of US stocks was highlighted by UK asset manager Schroders in its Equity Lens report for August 2023.

Schroders strategic research unit said in the report: “The Super-7 US stocks now make up more of MSCI ACWI than Japan, UK, China and France combined. The rest of the world has been left in their wake this year.”

Source: Schroders.

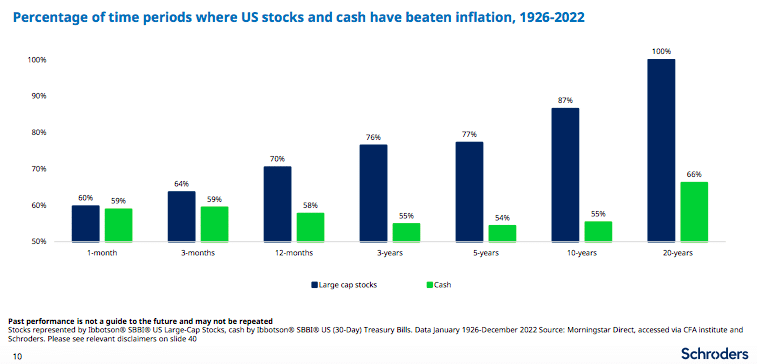

Schroders also argued that in the long-run, stock market investing wins out over cash.

Source: Schroders.

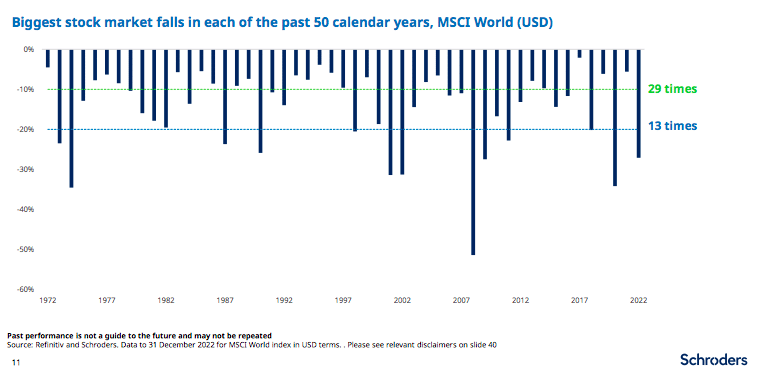

However, the asset manager said it can be a bumpy ride as 10% falls often happen in a year.

Source: Schroders.

The source paper used by Datatrek can be read here: “Long-term shareholder returns: Evidence from 64,000 global stocks” (Bessembinder, Chen, Choi, Wei, revised 2023): https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3710251

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

It's been a month since we had our Women In Finance Awards in New York City at the Plaza! Take a look back tab some moments, and nominate for our upcoming awards in Mexico City and Singapore here: https://www.marketsmedia.com/category/events/

4Citadel Securities told the SEC that trading tokenized equities should remain under existing market rules, a position that drew responses from various crypto industry groups. @ShannyBasar for @MarketsMedia:

SEC Commissioner Mark Uyeda argued that private assets belong in retirement plans, saying diversified alts can improve risk-adjusted returns and that the answer to optimal exposure “is not zero.” @ShannyBasar reporting for @MarketsMedia:

COO of the Year Award winner! 🏆

Discover how Jennifer Kaiser of Marex earned the 2025 Women in Finance COO of the Year recognition.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

DeFi has secure access to equities data including after-hours and overnight sessions for the first time.

-

ICE’s derivatives markets and its equity markets at NYSE set multiple milestones in 2025.

-

The new venue will support trading of tokenized shares that are fungible with traditional securities.

-

The suite had record futures and options average daily volume and open interest last year.

-

The equities on OPEN will trade on Figure’s ATS, opening the door for continuous trading.