Decentralised finance (DeFi) has emerged as a fast-growing segment within the cryptoasset ecosystem. DeFi is an umbrella term commonly used to describe a variety of services in cryptoasset markets that aim to replicate some functions of the traditional financial (TradFi) system, purportedly by disintermediating their provision and decentralising their governance. In DeFi, the role of financial institutions and market infrastructures is replaced to varying degrees by self-executing code, or so-called smart contracts.1

The turmoil in cryptoasset markets and in DeFi in 2022 exposed a number of vulnerabilities in relation to DeFi, including operational fragilities and liquidity and maturity mismatches, as well as issues relating to leverage and interconnectedness. So far, these vulnerabilities have not affected the traditional financial system due to DeFi’s relatively small size and limited interconnectedness with traditional markets. However, the scale of DeFi and/or its links with TradFi may grow over time, raising the potential for contagion and threats to financial stability.

Against this background, the Financial Stability Board (FSB) published a report in 2023 entitled The Financial Stability Risks of Decentralised Finance to provide an overview of the main features and vulnerabilities of DeFi, assess potential financial stability threats and draw policy implications.

Background of DeFi

DeFi services are built in a multi-layered architecture that includes permissionless blockchains,2 smart contracts, DeFi protocols3 and purportedly decentralised applications (DApps). DApps can replicate some functions of the traditional financial system. These include decentralised exchanges (DEXs), decentralised forms of lending, derivatives issued and traded in a decentralised system, initial forms of decentralised insurance and asset management.

The DeFi ecosystem is a complex web of interconnections involving multiple players with varying interrelationships and interests. They include protocol creators and developers, so-called decentralised autonomous organisations (DAOs),4 funders (eg venture capital and private equity funds) and institutional and retail end users, among others. DApps purport to have decentralised ownership and governance structures if they have such structures at all. However, in some DeFi applications, decision-making is centralised and, in practical terms, the actual degree of decentralisation among underlying DeFi organisational structures varies broadly.

The DeFi market is driven largely by institutional participants in advanced economies. In contrast, there is relatively little direct participation from retail investors and emerging or low-income economies. To date, DeFi is mainly self-referential, in the sense that DeFi products and services interact mainly with other DeFi products and services rather than with TradFi and the real economy.

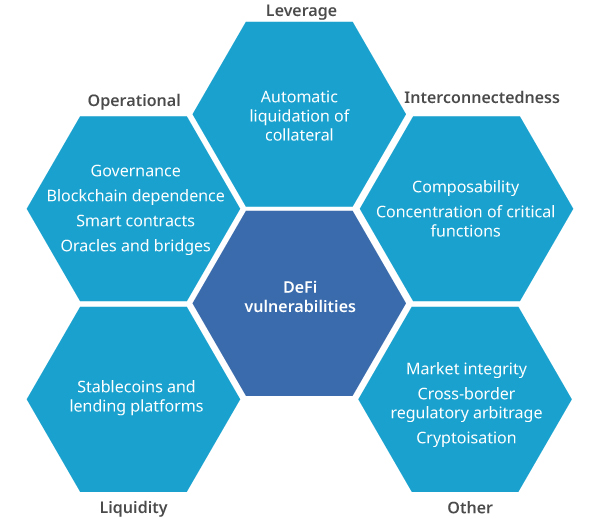

DeFi vulnerabilities, interlinkages and transmission channels

While the processes to provide services are in many cases novel, DeFi does not differ substantially from TradFi in the functions it performs. In attempting to replicate some of the functions of the TradFi system, DeFi inherits and may amplify the vulnerabilities of that system. This includes well-known vulnerabilities relating to operational fragilities, liquidity and maturity mismatches, leverage and interconnectedness.

However, DeFi’s specific features may result in these vulnerabilities sometimes playing out differently than in TradFi, for example as a result of spillover effects related to the automatic liquidation of collateral based on smart contracts or dependence on the underlying blockchain. The amplification of known vulnerabilities comes from novel technological features, the high degree of structural interlinkages amongst the participants in DeFi and from non-compliance with existing regulatory requirements or lack of regulation.

The extent to which DeFi vulnerabilities can lead to financial stability concerns largely depends on the interlinkages and associated transmission channels between DeFi, TradFi and the real economy. These channels include financial institutions’ exposures to DeFi; confidence and wealth effects stemming from the involvement of households and firms in DeFi; and the extent to which DeFi applications may facilitate the use of cryptoassets for payments and settlement. To date, these interlinkages are limited, as shown by the modest impact of the 2022 cryptoasset market turmoil on TradFi.

Conclusions

In future, one plausible scenario is that DeFi continues to grow and becomes more interconnected with the real economy and the broader financial system. Thus, the FSB report highlights the need to carefully monitor vulnerabilities inherent in DeFi and potential threats to financial stability which is hampered by the absence or low quality of available data, the lack of or non-compliance with reporting requirements, and market practices oriented towards operating in opaque and non-transparent ways.

In the light of these findings, the FSB report puts forward several considerations for future work. First, the FSB will proactively analyse the financial vulnerabilities of the DeFi ecosystem as part of its regular monitoring of the wider cryptoasset markets. Second, the FSB, in collaboration with regulatory authorities and other standard-setting bodies, will explore approaches to measure and monitor DeFi interconnectedness with TradFi. Third, as both the use cases and regulatory approaches around DeFi are still evolving, the FSB will explore the extent to which its proposed policy recommendations for the international regulation of cryptoasset activities may need to be enhanced to take account of DeFi-specific risks and facilitate the enforcement of rules.

- A smart contract is a cryptoasset term that refers to self-executing applications that can trigger an action if some pre-specified conditions are met.

- A blockchain is a form of distributed ledger in which details of transactions are held in the ledger in the form of blocks of information. A block of new information is attached into the chain of pre-existing blocks via a computerised process by which transactions are validated. A permissionless blockchain allows anyone to access the network and participate in the validation of transactions, while a permissioned one allows only a pre-selected group of participants to access the network and validate transactions.

- A DeFi protocol is a specialised system of rules that creates a program designed to perform traditional financial functions.

- A DAO is, in theory, a decentralised application consisting of rules of operation that dictate who can execute a certain action or make an upgrade. Code helps create an organisational structure intended to function without a centralised management structure.

This Executive Summary and related tutorials are also available in FSI Connect, the online learning tool of the Bank for International Settlements.

Source: BIS

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

As Technology Evolves, Asset Managers Adapt and Innovate

https://www.marketsmedia.com/as-technology-evolves-asset-managers-adapt-and-innovate/

Citi Changes Organizational Structure

https://www.marketsmedia.com/citi-changes-organizational-structure/

SEC Charges Virtu for Disclosures Relating to Information Barriers

https://www.marketsmedia.com/sec-charges-virtu-for-disclosures-relating-to-information-barriers/

ICE Futures Singapore Partners with CoinDesk Indices

https://www.marketsmedia.com/ice-futures-singapore-partners-with-coindesk-indices/

Related articles

-

Verifying identity on-chain lowers one of the barriers to entry to DeFi for traditional institutions.

-

For the first time, holders of tokenized real-world assets can natively use their assets onchain.

-

The protocol facilitates compliant access to DeFi for institutional users.

-

Recommendations aim to mitigate risks to investors, market integrity & combat illicit finance.

-

Traditional finance derivatives are being replicated in digital assets.